Building on last year’s Season 1 strategy 1 post, the following is a proposed product roadmap that reflects changes in a market that looks very different from just six months ago as well as new product concepts now being surfaced.

North Star = Zero DOLA Bad Debt

First, the DAO’s “north star” remains zero DOLA bad debt. We’re making steady progress in this regard but there is more work to do and we propose three initiatives for getting us there even faster:

sDOLA everywhere

INV everywhere

FiRM 2.0

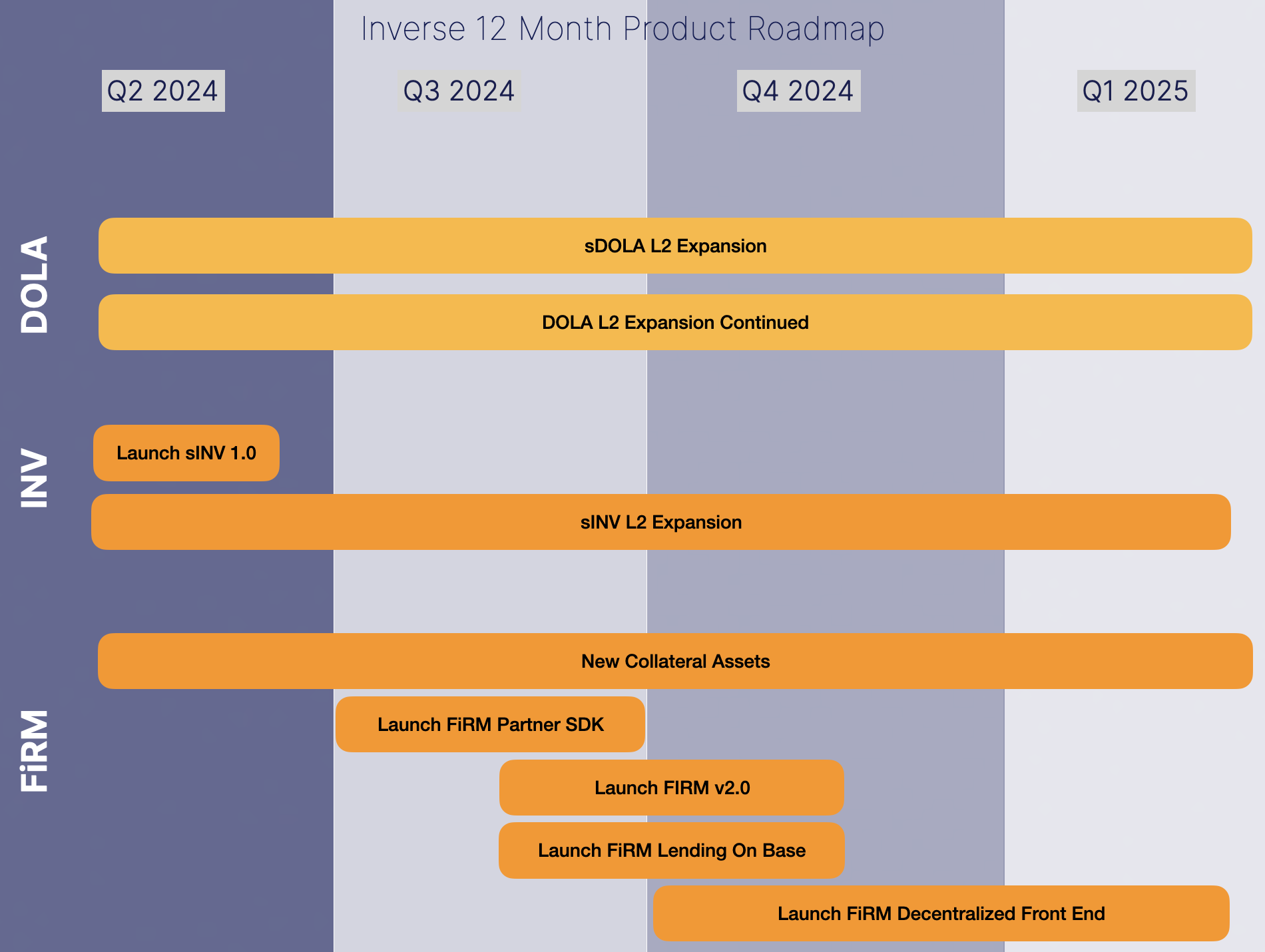

1. sDOLA Everywhere

sDOLA is, we believe, the most elegant decentralized yield-bearing stablecoin on the market today. sDOLA is free of compromises with US treasuries, centralized custodians, and uses no governance tokens as a yield source. While many formerly “decentralized” stablecoin projects are now flirting with or totally shacking up with centralization, we believe a “fully organic” approach to yield is in the best long-term interests of everyone, addresses an important segment of the market that is skeptical of centralization, and further highlights the DAO’s positioning with decentralization as a pillar of who we are.

sDOLA is also an essential pillar to the future growth of lending on FiRM. As sDOLA demand increases, it means sDOLA is being locked instead of swapped for another token, which has the effect of increasing DOLA lending capacity on FiRM. As we lend more DOLA, that translates into increased revenues for the DAO, more DBR issuance to INV stakers, and as DBR is spent on FiRM loans, more yield for sDOLA holders.

An area of exploration for sDOLA is the potential to automate aspects of DBR issuance to allow for DBR price and DBR burn, rather than a flat number set by governance, to determine the amount of DBR sent to sDOLA stakers. This would also have the effect of adding further autonomy to sDOLA as we continue to seek new paths of immutability.

To-date, sDOLA’s liquidity picture is small relative to the robust DOLA liquidity picture. As sDOLA liquidity changes (and sDOLA TVL), the picture for FiRM and DAO revenues does too. To build sDOLA liquidity, we are going to bring sDOLA across multiple Ethereum L2’s during Season 2. By building partnerships with native DEX partners on new chains, we can build sDOLA liquidity with modest incentives from the DAO treasury that, if our partnerships with Aerodrome or Velodrome are any indicator, have great payoff potential.

A key deliverable for cross-chain sDOLA is our partnership with Chainlink and their Cross-chain Interoperability Protocol (CCIP). With CCIP in place, we will move aggressively to build new sDOLA liquidity, with DOLA and partner stablecoin pairs on those chains.sDOLA liquidity on existing L2’s including Base, Arbitrum, and OP mainnet are natural starting points, however a growing number of new Ethereum L2’s show great promise for DOLA and sDOLA, and establishing partnerships with trustworthy emerging networks will be a priority in terms of business development.

Beyond just liquidity driving sDOLA TVL, this move to bring sDOLA across chains also opens up avenues for sDOLA as collateral on third party lending protocols and perpetual futures markets.

While there are no immediate plans for DOLA Feds on these chains, our work to-date with DOLA Feds on Base, OP, and Arbitrum demonstrates the potential for scaling liquidity once the requisite risk, treasury, and other plumbing is in place. Part of our product strategy is to streamline the cross chain deployment process for cross chain feds, reducing overhead and allowing us to move quickly on emerging opportunities. Prospective L2 partners, noting our success with Aerodrome, Velodrome, and others are keen to see our model replicated on their chains, creating an opportunity for the DAO to, in effect, offer “Liquidity as a Service” to new DEX partners offering attractive veNFT and other incentive programs. Though only thoroughly vetted protocols should be considered for expansion to minimize risks.

sDOLA cross-chain deployment is imminent and L2 expansion to existing L2’s and new ones is a major thrust for the DAO for the next 12 months, accompanied in each case by cross-chain DOLA deployment.

2. INV Everywhere

Inverse is carving out an attractive quadrant of the DeFi lending market: long-term fixed rate lending and Today, INV is available on Ethereum mainnet and CEX’s like Coinbase, but in order to capture xINV anti-dilution and DBR streaming rewards, INV must be staked exclusively on Ethereum mainnet. Additionally, DBR streaming rewards are currently claimed manually, which can be inconvenient and require high gas costs.

We believe INV is a hugely important DeFi governance token due to our approach to a multi-billion dollar fixed rate lending market opportunity, and therefore INV should be available not just to mainnet users but to users on many chains. To offer INV staking on a cross-chain basis with our current approach to INV staking is technically difficult and replete with risk. Moreover the current approach does not address the “hassle” of manually claiming rewards.

A better way to bring INV across chains and introduce INV to wallets of all sizes is to offer a wrapped version of INV, called sINV, using an ERC-4626 vault (as we do today with sDOLA) that automatically captures DBR rewards and autocompounds them into a single token users can take with them anywhere, use as lending collateral, etc.

sINV has significant potential to add continuous buy pressure for INV as DBR designated for the sINV vault is continually swapped for INV, tightening the coupling between FiRM and INV.

As with sDOLA, that path to bringing sINV across chains is with Chainlink CCIP, which will ship this quarter (soon, actually). One caveat with sINV is that for now, governance rights for holders will be gone and to vote in governance will still require staking INV the way you do today on mainnet. This will be addressed in a future governance overhaul, but is deemed as a low priority for the next 12 months.

Worth mentioning is that the L2 expansion described above for sDOLA and DOLA applies to sINV. Thus in addition to increased demand for INV, we will also see deeper all-chain liquidity (and volumes) for INV, which brings with it additional benefits.

This initiative for sINV is already underway and should be live in a matter of weeks:

3. FiRM 2.0

The DAO has built something truly innovative with FiRM and to-date there are no direct rivals offering long-term, fixed rate, non-custodial lending on any chain. We believe fixed rate lending is the future of DeFi and we will continue to innovate, bringing new features to FiRM as well as bringing direct DOLA lending via FiRM on one or more new chains. For the sake of simplicity, we call this set of initiatives “FiRM 2.0.”

New Collateral Assets

Not a new feature or product, but we can prudently but regularly evolve whitelisted collateral assets for FiRM to reflect user demand, improve safety, and towards sustained TVL growth.

Currently we are evaluating a range of new collateral including:

New yield bearing tokens including LST’s and LRT’s

LP tokens, initially DOLA stable pairs.

Memecoins

FiRM Partner SDK

We are in early discussions with developers who seek to provide “white label” access to fixed rate lending to their users without surfacing today’s FiRM UX. We will provide an abstraction layer to assist developers who want to help bring FiRM everywhere. This is primarily a UI toolkit and documentation and should have minimal impact on our smart contract dev resources.

New FiRM Features

A backlog of feature requests for FiRM will result in a series of feature improvements to the way we conduct liquidations and fetch oracle prices on FiRM.

Liquidations

For example, in terms of liquidations, we are planning multiple improvements for the FiRM liquidation engine. Instead of treating every loan and borrower identically, applying flat liquidation fees and liquidation factors, our updated liquidation engine will use models that allow us to reduce fees and factors for less risky loans, and increase them for riskier loans. These changes will ultimately allow our risk team to propose more attractive parameters for markets, increasing the utility of borrowing on FiRM. Finally we hope to increase the gas efficiency of liquidations, to make their execution as efficient as possible.

Oracles

In terms of oracles, we plan to update our pessimistic oracle to be even more robust along with adding features such as operation specific oracle price, which allows valuing collateral differently depending on the market action that is being taken and adding fallback price feeds directly in the oracle to protect against black swan events.

FiRM on Base

DOLA’s liquidity position on Base combined with high user demand for DOLA loans on Base have shifted the goal of deploying FiRM on OP mainnet to Base, where TVL growth is rapid and the opportunity to address the Coinbase installed base with fixed rate loans is large. Note that if borrow capacity allows and we see borrow demand on OP mainnet, there is little reason not to also expand there as well.

Unlike some lending markets where cross-chain deployment is comparatively simple, technical issues like how to issue DBR to INV stakers on Base make deploying FiRM cross-chain more resource intensive. Still, this is a roadmap priority over the next 6-12 months for the DAO.

Decentralized Frontend for FiRM

The DAO should begin the process of decentralizing the FiRM frontend. There are varying approaches and open questions about compensating front end providers, but we are in an era where decentralization of lending and stablecoin project frontends is a competitive advantage and eliminating this point of centralization in the protocol removes a risk vector for the DAO.

Final Thoughts

The above is a 12-month roadmap that, if the DAO’s history is a guide, will need to respond to rapid shifts in the marketplace. Mostly this roadmap iterates on existing product lines and continues to focus the DAO on exploiting our competitive advantage in them vs. introducing a completely new product. Given the size of the fixed rate lending market and DAO resource constraints today, the scope of the roadmap is practical but also very powerful in terms of returning value to INV holders over the coming months.

Finally, it’s worth mentioning that the level of innovation and new ideas being informally or semi-formally discussed among contributors and DAO members is nothing short of exhilarating. And none of these are reflected in this roadmap but upon further due diligence may be surfaced during the next 6-12 months. Maybe sooner.

As always, your ideas are welcome. LGTM.